Housing market’s summer surge dampened by soaring stamp duty costs

-

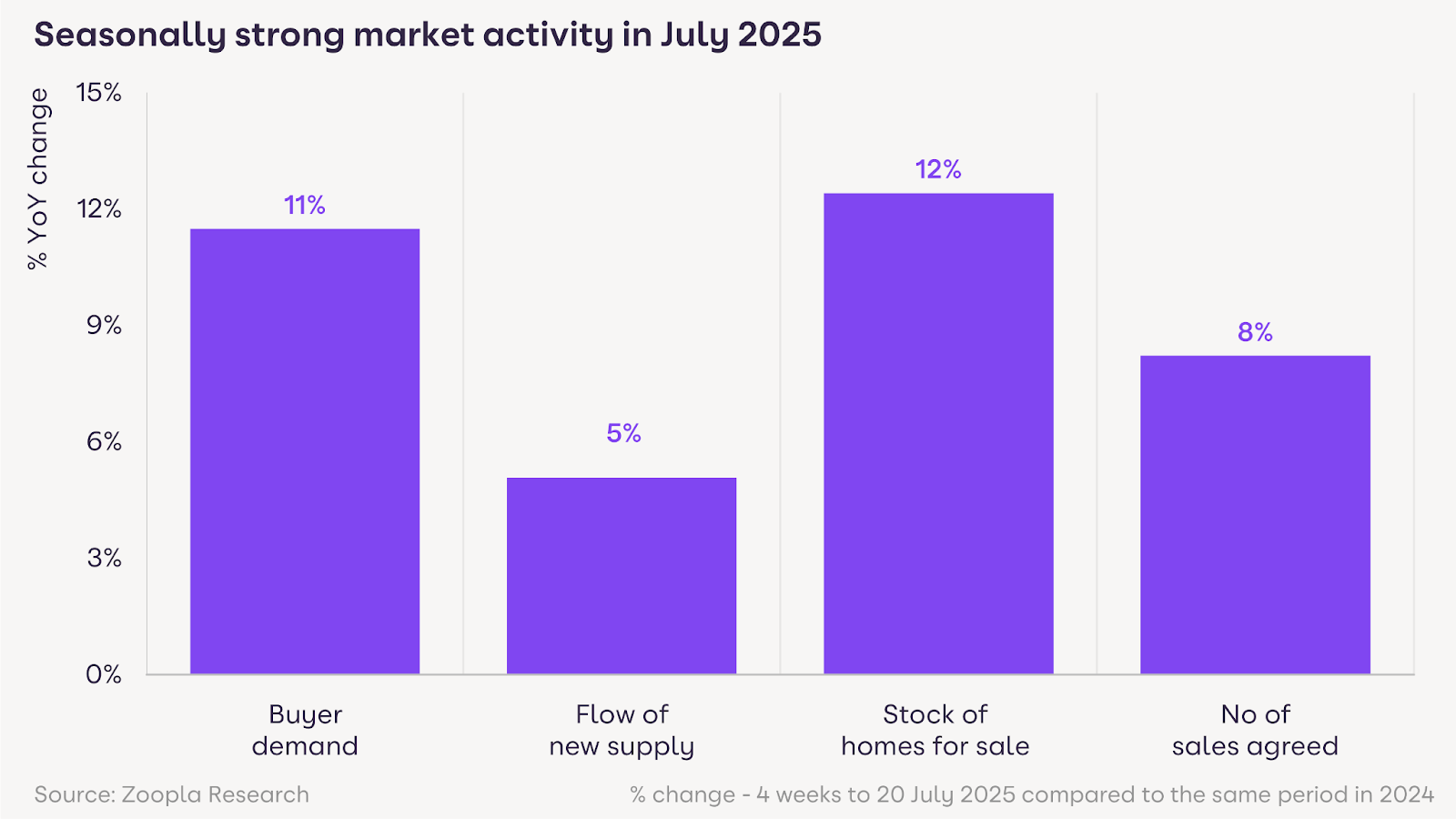

Housing market activity has surged, with buyer demand up 11 per cent and agreed sales up eight per cent year-on-year, defying typical summer slowdown

-

National house price inflation has slowed to 1.3 per cent, driven by a 12 per cent increase in homes for sale and higher stamp duty costs for many buyers

-

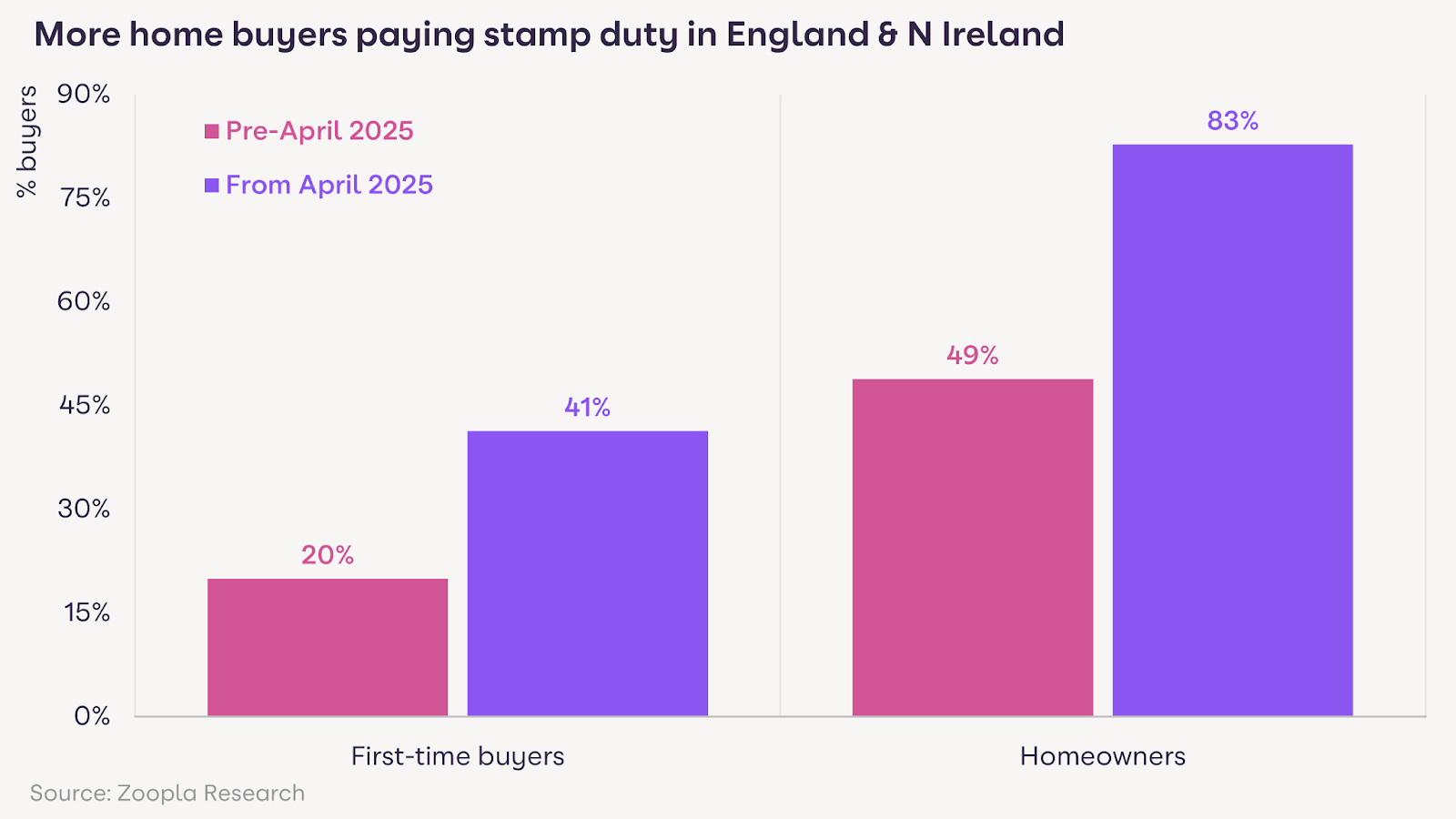

Higher stamp duty costs now impact 83 per cent of homeowners and 41 per cent of first-time buyers (up from 19 per cent), with the impact on prices felt primarily in Southern regions such as London and the South-East

-

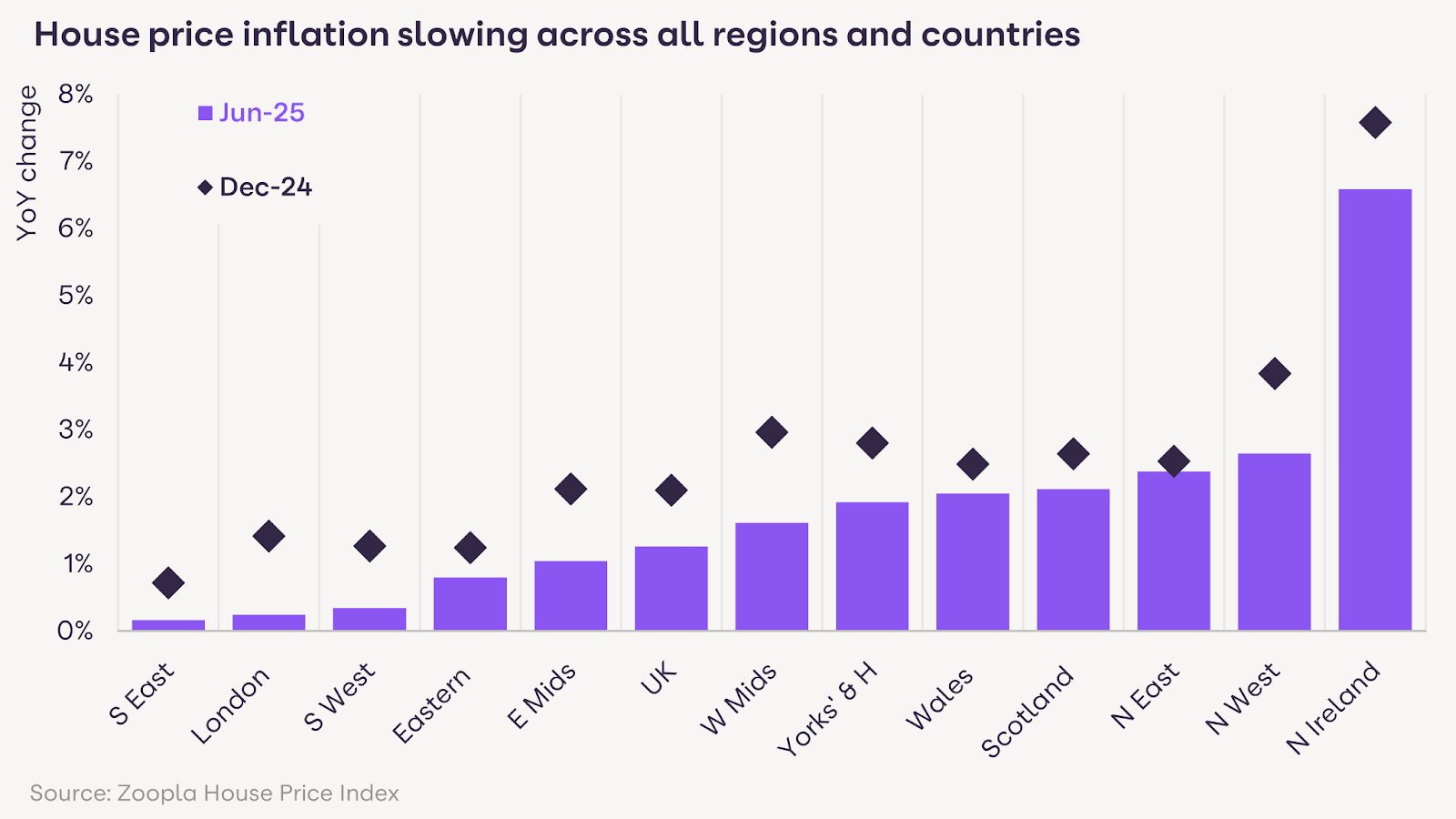

Northern England, Scotland and Wales are seeing faster price growth (two to three per cent), with Northern Ireland at 6.1 per cent. Southern England is seeing the weakest growth (below one per cent)

-

Truro, Torquay and Exeter are registering some of the biggest price falls outside of London, at -1.3 per cent, -1.2 per cent and -1.1 per cent respectively

-

Zoopla anticipates five per cent more sales in 2025 than last year, but price growth is expected to remain in low single digits, a downward revision from the previously forecasted two per cent to one per cent

Activity in the housing market is stronger than it was 12 months ago, defying the usual seasonal slowdown seen during the summer. This is according to Zoopla’s latest House Price Index. Buyer demand is 11 per cent higher, accompanied by an eight per cent increase in agreed sales1. There are currently a record number of homes on the market, an average of 37 per estate agent branch, with more buyers actively looking to finalise deals before the start of the school holidays and the August slowdown.

Recent changes to the way lenders assess mortgage affordability have been a catalyst for the increased activity. Home buyers using a mortgage can now borrow up to 20 per cent more, at the same rate, than they could just three months ago. This has encouraged more buyers to try and secure a home purchase before the summer and is why buyer demand and sales agreed are higher across all regions and countries of the UK.

Table 1: Seasonally strong market activity in July 2025

Higher stamp duty costs create a drag on price inflation

While the market is seeing increased activity, higher stamp duty costs in England and Northern Ireland, following the end of temporary reliefs in April, are creating a significant drag on price inflation. A total of 83 per cent of homeowners now pay stamp duty on new purchases, compared to less than half (49 per cent) before April 2025. The extra cost is up to £2,500 per sale, around one per cent of the average UK home price. Buyers will be looking to reflect these increased buying costs in what they offer for homes, ultimately impacting agreed sale prices.

Stamp duty costs also vary between existing homeowners and first-time buyers. Given that it is a tax based on property value, stamp duty costs have a greater impact on buyers in southern England more than other areas, contributing towards an additional drag on price inflation. First-time buyers are charged lower rates and tend to buy cheaper homes, however 41 per cent are now liable for stamp duty compared to just 19 per cent before April 2025. The greatest impact is on those buying in London and higher value parts of the South East. Based on the average first-time buyer price in London the stamp duty cost is £6,100 compared to £0 before April.

Table 2: More home buyers paying stamp duty in England & N Ireland

UK house price inflation slows as buyers market continues

In addition to the effects of higher stamp duty costs, the growth in the number of homes for sale is contributing to the slowdown in UK house price inflation.

Zoopla’s house price index reveals the annual rate of price inflation has now fallen to just 1.3 per cent, with the average UK house price sitting at £268,400, a modest £3,350 increase from a year ago. This national slowdown comes despite increased market activity and reflects a major shift, with a 12 per cent increase in national housing supply re-enforcing the buyer’s market, boosting choice and keeping offers competitive. Although price growth is up from 0.4 per cent last June, it has nearly halved from the 2.1 per cent seen just six months ago in December 2024.

Table 3: House price inflation slowing across all regions and countries

While the overall pace of growth has nearly halved from 2.1 per cent from six months ago, regional disparities are stark. Northern regions of England, Scotland, and Wales are experiencing faster house price inflation, typically between two to three per cent annually. Northern Ireland is a standout, with prices up 6.1 per cent, 7.8 per cent in Belfast, albeit from a lower base. In contrast, southern regions of England are seeing the weakest price inflation, consistently below one per cent. This ranges from 0.2 per cent in the South East and London to 0.3 per cent in the South West. Truro, Torquay and Exeter are registering some of the biggest price falls outside of London, at -1.3 per cent, -1.2 per cent and -1.1 per cent respectively.

Table 4: Top five areas with the highest and lowest House Price Inflation

|

Price Risers |

|||

|

Postal Area |

Dec-24 |

Jun-25 |

Average price |

|

BT – Belfast |

7.8% |

6.1% |

£186,500 |

|

HX – Halifax |

3.5% |

4.2% |

£175,900 |

|

FK – Falkirk |

3.5% |

3.6% |

£167,500 |

|

ML – Motherwell |

5.3% |

3.6% |

£132,000 |

|

TD – Tweeddale |

0.4% |

3.6% |

£176,000 |

|

Price fallers |

|||

|

Postal Area |

Dec-24 |

Jun-25 |

Average price |

|

EX – Exeter |

0.0% |

-1.1% |

£308,800 |

|

TQ – Torquay |

-1.1% |

-1.2% |

£293,700 |

|

TR – Truro |

0.3% |

-1.3% |

£314,400 |

|

W – West London |

0.8% |

-1.5% |

£768,900 |

|

WC – WC London |

-1.2% |

-5.0% |

£823,000 |

Source: Zoopla HPI June 2025

Commenting on the report, Richard Donnell, Executive Director at Zoopla, said: “The housing market is broadly in balance. We’re seeing healthy levels of demand and sales, but this isn’t sparking faster price inflation. In fact, more homes for sale, particularly across southern England, is re-enforcing a buyer’s market, keeping price rises in check. Many more home buyers are paying stamp duty since April and want this extra cost reflected in the price they pay. While mortgage rates are holding steady, less stringent affordability testing has boosted buying power and is supporting more sales despite increased uncertainty.

“At the start of the year, we predicted house prices would rise just two per cent, at the lower end of forecasts for house price inflation. Prices are on track to be one per cent higher over 2025, half the level forecast. Greater supply of homes for sale and mortgage rates remaining higher than expected are the key reasons for weaker growth. Low house price inflation is not a bad thing so long as there is enough market confidence for people to list their homes and make bids to buy homes.”

David Powell, CEO Andrews Property Group, added: “The market is continuing to find its new normal since the stamp duty incentive was withdrawn at the end of March 2025. In addition businesses are coming to terms with the increases in National Living Wage and National Insurances. The market continues to show incredible resilience, however the slow down in house prices is starting to impact consumer confidence illustrated by the increased numbers of properties currently on the market for sale.

“Without a reduction in interest rates or Government intervention its difficult to see any material change for H2. The obvious and immediate route is to create a more palatable and permanent solution to stamp duty to help ignite the market. The Government will certainly need a more flamboyant market to provide confidence to developers to build towards the targeted 1.5 million homes. The affordability challenge to buyers remains and I would advocate for immediate remedies to help consumers buy with confidence.”

You May Also Enjoy

Are landlord repossessions set to spike ahead of RRA?

Breaking Property News 23/2/26

Volume doubles as property market sees strong return of new applicants

Property valuation leads to agents up 50% on last year

Worst areas for landlord eviction waiting times