Sales agreed up 12% on last year despite annual mortgage costs 61% higher than 2021

-

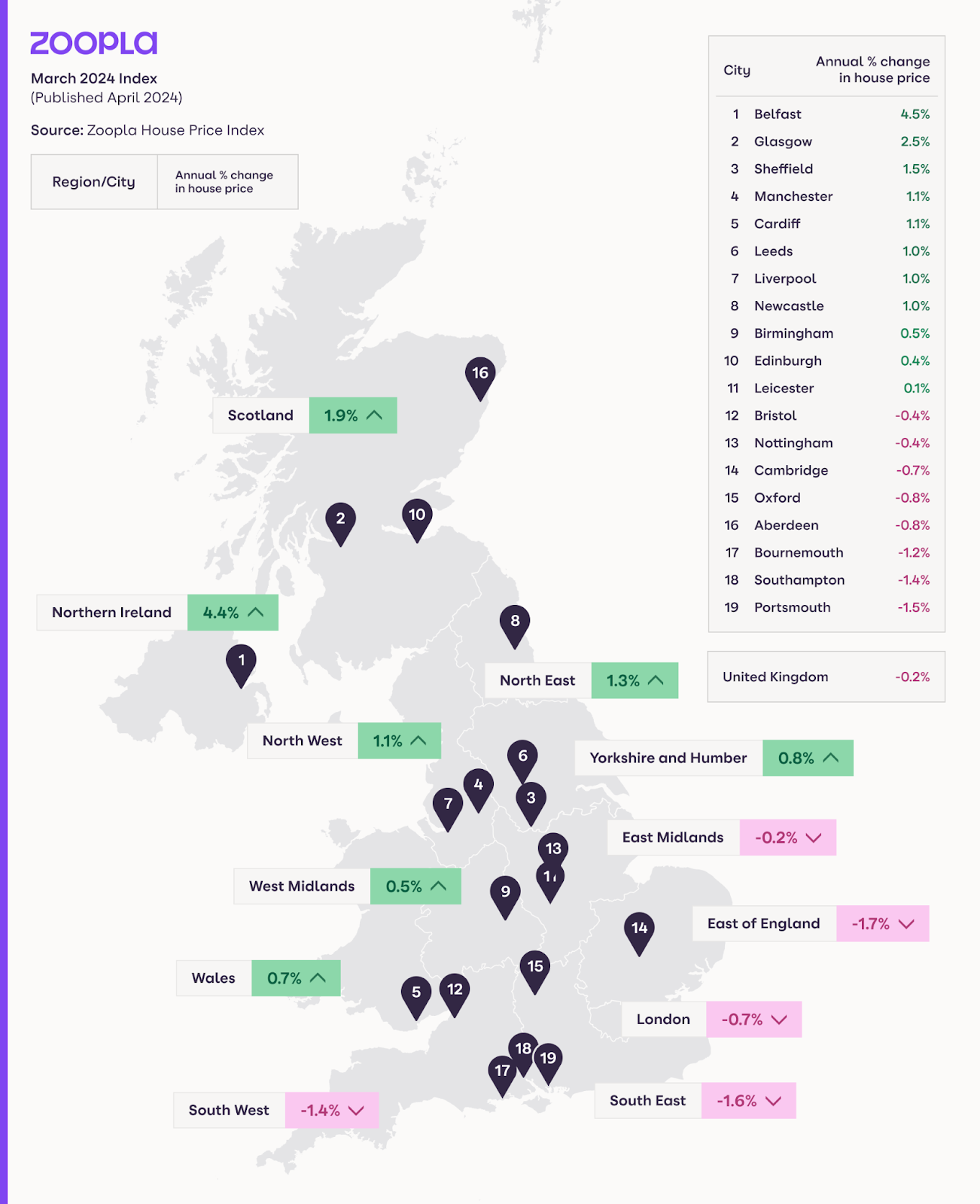

UK house prices broadly static but sales volumes are up 12% year on year

-

UK house price inflation unchanged from last month at -0.2%

-

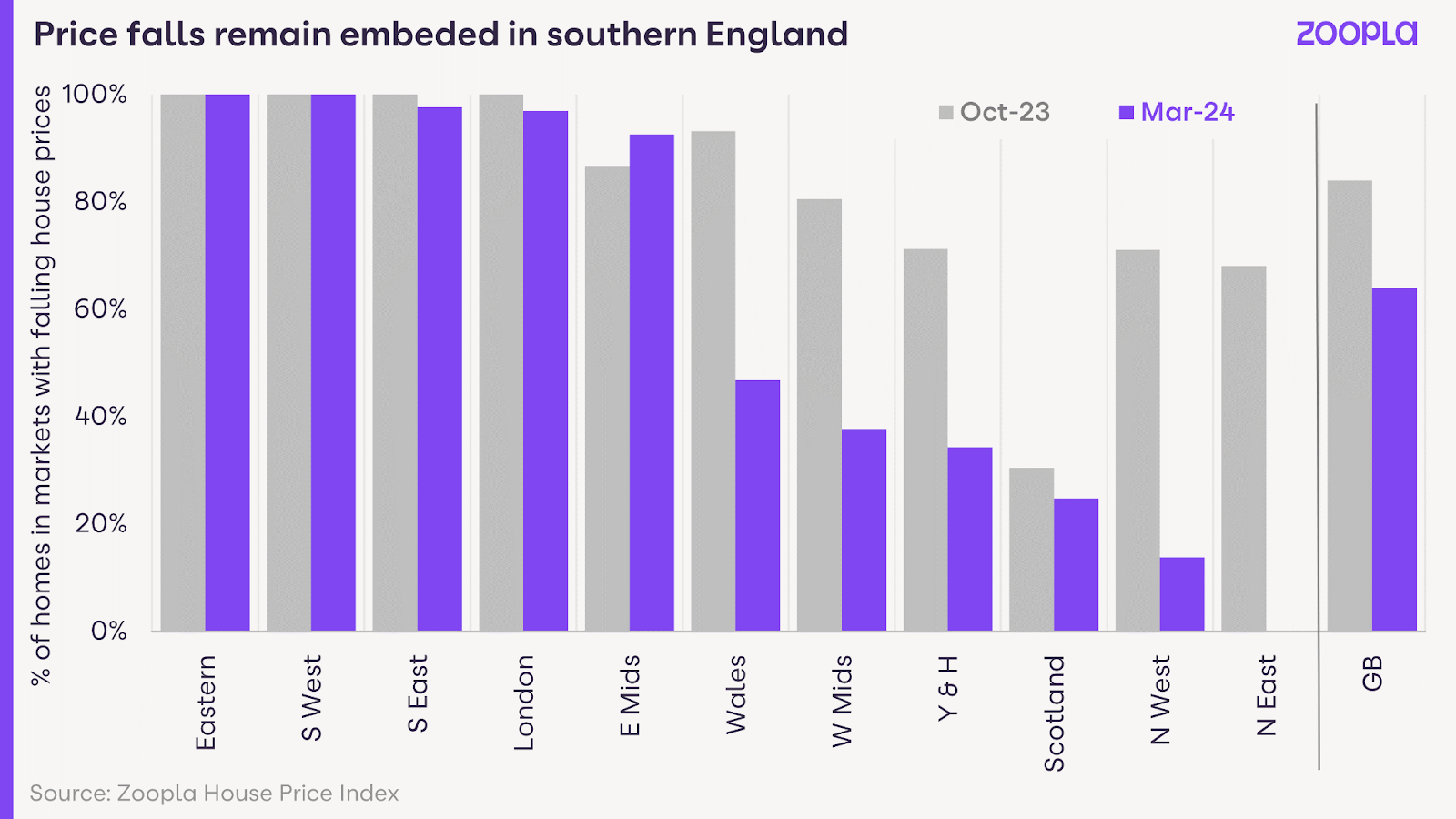

Almost two thirds (64%) of all homes are in local markets with annual price falls, down from 82% last October with a clear north-south divide emerging.

-

Higher mortgage rates continue to impact buying power and drag on price growth

-

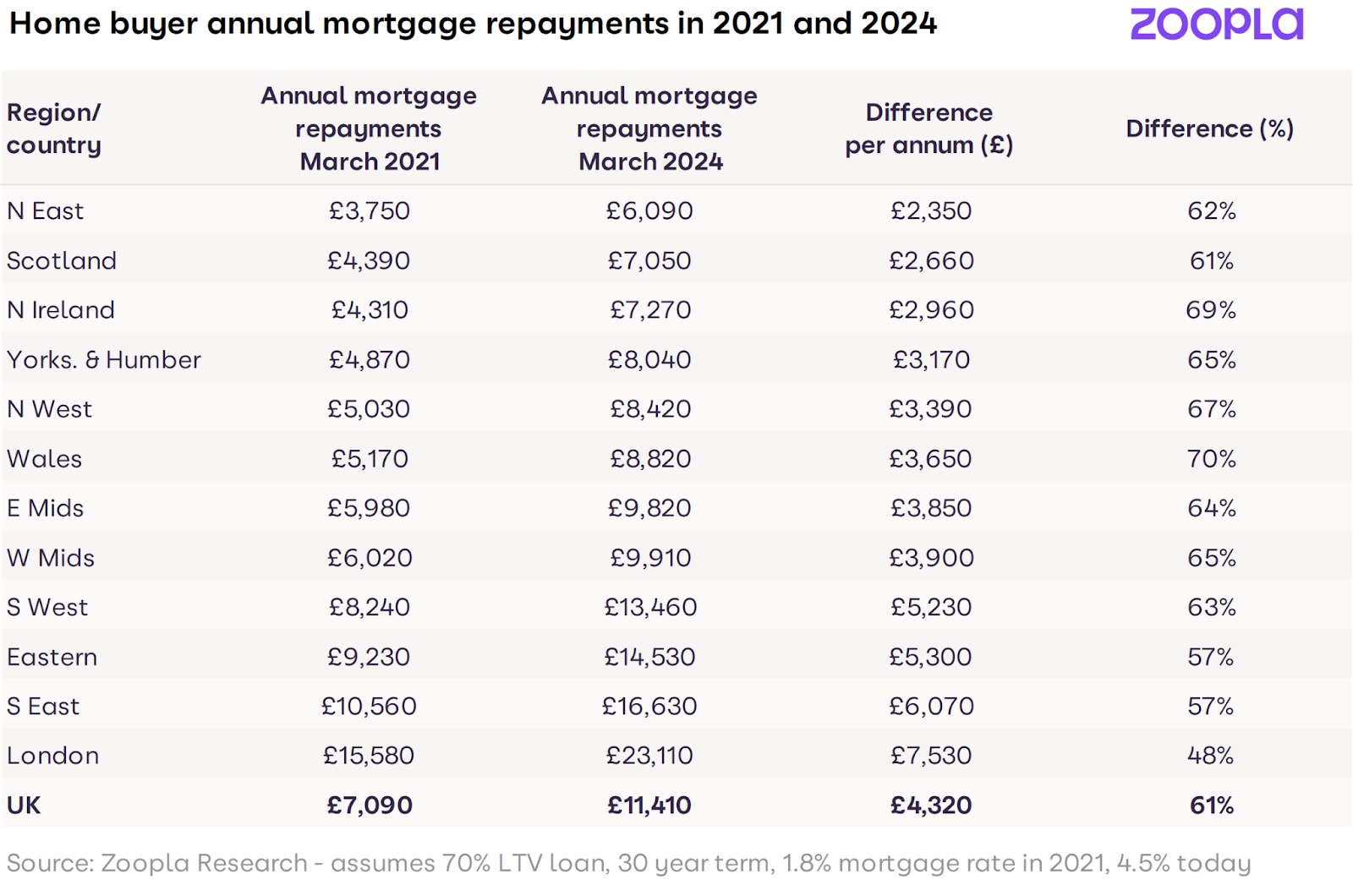

Annual mortgage repayments for a typical home buyer are 61% higher than 3 years ago – two thirds is down to higher mortgage rates and one third due to higher house prices

-

Higher mortgage rates and other buying costs like stamp duty are behind ongoing price falls across southern England

-

The market is on track for 1.1m sales in 2024, up 10% on last year

UNDER EMBARGO UNTIL 00.01 MONDAY 29TH APRIL, LONDON: More homes for sale and renewed confidence amongst buyers continues to support the number of sales being agreed which are 12% higher compared to this time last year1, reveals property website Zoopla.

The latest monthly House Price Index also shows that UK house price growth remains broadly flat (-0.2%) contributing to a more balanced market, meaning more people have the chance of moving home in 2024. Zoopla expects 100,000 more sales this year than in 2023 (1.1m in 2024 versus 1m in 2023) so long as sellers continue to remain realistic on pricing.

Mortgages repayments are still 61% higher impacting buying power

This positive increase in sales is beginning to reflect in other data such as mortgage approvals for home purchase which were 32%2 higher in February 2024 compared to the previous year, marking a return to pre-pandemic levels.

However, despite improving consumer confidence mortgage rates remain around 4.5% compared to sub 2% in March 2021. Higher mortgage rates are adding to affordability pressures for buyers and this is acting as a drag on house price inflation.

The average home buyer using a 70% loan to value mortgage faced annual mortgage repayments that are 61% higher today3 than three years ago (March 2021) before mortgage rates started to rise – in monetary terms the annual mortgage repayments have risen from £7,100 to £11,400.

Two thirds of this increase is driven by higher mortgage rates, but a third is down to the fact that house prices are 13% higher than 3 years ago. (March 2021).

But higher mortgage rates hit southern England hardest

At a regional and country level there has been a 50% to 70% increase in mortgage repayments for a typical buyer between 2021 and 2024 with the largest monetary impact felt in southern England where house prices are simply higher.

The annual cost of mortgage repayments for an average priced home is more than £5,000 a year higher in 2024 than 2021 across the South West, South East and East of England.

This rises to a high of an extra £7,500 in London. Across other regions and countries of the UK, the increase is lower, ranging between £2,350 and £3,900 a year.

While underlying household incomes will vary by area, lower mortgage increases are one reason that market activity and prices are holding up better in more affordable markets with lower house prices.

6 in 10 homes in markets registering annual price falls

The squeeze on housing affordability from higher mortgage rates, lower income growth and rising living costs is keeping house prices in check across southern England. Analysis of Zoopla’s granular local authority house price indices reveals that 64% of all homes are in markets still registering annual price falls4. This is lower than the 82% recorded last October with the scale of these price falls being relatively modest – in most cases between 0% and -3%.

The coverage of homes in markets with price falls is greatest across southern England where 95-100% of homes are now in local markets with annual price falls. The East Midlands also has a high proportion of markets with price falls at 93%.

Across the rest of Great Britain there are signs of improvement in pricing, with a decline in the proportion of homes in local markets with annual price falls across six regions. Scotland has pockets of lower prices but at a national level, prices haven’t fallen year on year. As the UK’s most affordable region with an average price of £142,000, the North East now has no areas with annual price falls.

Commenting on the latest report, Richard Donnell, Executive Director at Zoopla says: “The rebound in sales being agreed continues for a fourth month as mortgage rates have fallen, consumer confidence improves and home buyers have much greater choice of homes for sale. The pipeline of sales is growing and we expect 100,000 more people to move home in 2024 than last year.

There is clear evidence that house prices are firming and the pace of price falls is slowing. We don’t believe that prices will start to rise as buyers face much higher mortgage repayments than in the recent past. The market is adjusting to higher borrowing costs and what we need is continued price stability which will create the environment for continued growth in sales and home moves. It’s important sellers remain realistic on what they can achieve for their home. ”

You May Also Enjoy

Homebuyers face longer buying timelines

Breaking Property News 1/4/26

What renters and landlords need to know ahead of major rental law changes

Tackling Empty Properties

Pet-friendly rentals plunge 39%